February 2022 Property Data Breakdown

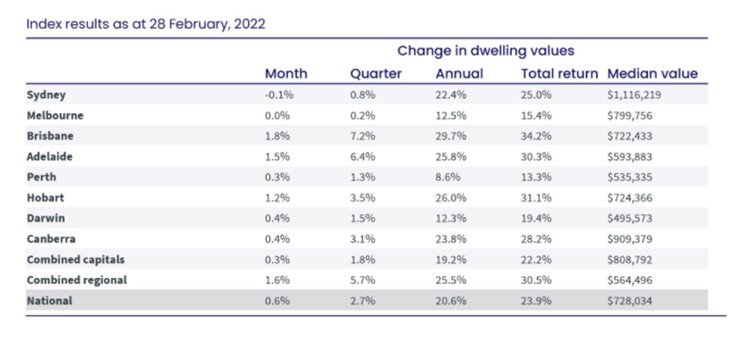

For the month of February, Core Logic has reported a national increase in the home value index of 0.6% nationally. This marks the lowest monthly growth reading since October 2020. January 2022 saw 1.1% nationally and the peak over the last 17 months was March 2021 with 2.8%.

As per CoreLogic’s Director of Research Tim Lawless, all capital cities are now recording a trend of slowing dwelling value growth, some capital cities being far more significant than others.

The sharpest slow downs were experienced in Sydney with -0.1% growth, being Sydney’s first decline since September 2020, and Melbourne sitting flat at 0.00%.

The capital cities with the least amount of impact were Brisbane with 1.8% growth, Adelaide with 1.5% growth and Hobart with 1.2% growth. 5 of the 6 regional markets also saw gains that were more than 1.2%.

As per core logic February 2022.

Looking at the quarterly figures it is evident in the divide in capital cities highlighting that the Australian Property Market is not just one market. Brisbane in top spot with 7.2% growth for the quarter, Adelaide in second place with 6.4% growth for the quarter and Melbourne just 0.2% higher along with Sydney values at 0.8% higher over the last 3 months.

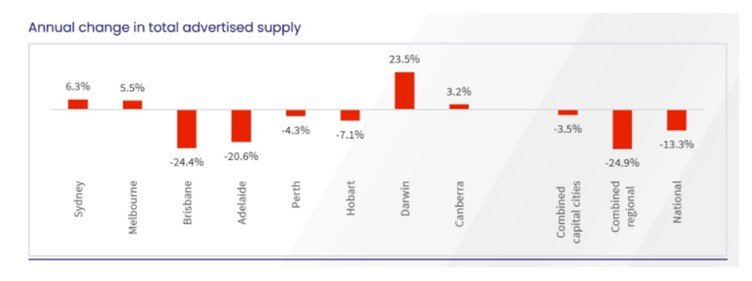

Nationally, the number of properties advertised over the 4 weeks to the 27th of February was 13.3% lower then the same period 12 months ago. This showcases lower stock levels and lower supply on a macro level.

Brisbane and Adelaide are experiencing stock levels more than 20% lower now than 12 months ago and 40% lower than the 5-year average. This supply issue being a factor in continued growth across Brisbane and Adelaide.

Sydney and Melbourne are seeing stock levels begin to normalize. This can be attributed to newly listed properties coming to market along with softening demand due to affordability issues.

As per core logic February 2022.

Although housing values softened nationally, rental growth is holding firm with a stabilized national growth rate of 3.2%. Sydney sitting at 2.4% and Melbourne sitting at 2.8%, having the lowest yield profiles, however seeing a slight increase for the month.

Tim Lawless believes that we could be seeing the bottom of the cycle for rental yields. Over the last couple of years historic low rental yields were experienced in several capital cities. If rents continue to rise faster than housing values, which is a strong possibility for Sydney and Melbourne this will see an improvement in yields.

In Brisbane and Adelaide, where house values are growing fasting than rent prices, it’s likely we could see yields compress to record lows. Even with this trend occurring, the yields are far stronger than comparison cities of Sydney and Melbourne.

It’s important to keep in mind that although the trend of markets across capital cities has seen a decline in growth, this does not mean that all capital cities will not see further growth. It’s not sustainable to continue to do 30% in a 12-month period. This decline in growth may mean that we could see some markets continue to perform at 10% ,15% or even 20% in the following 12 months. If this is the case these amounts of growth are still great results.

Remember that the Australian property market is made up of many mi markets and is not one market as much as the main-stream media would like you to believe. Ensuring you select markets that are at the early stages of their growth cycle is key.

If you have any questions regarding this month’s property data or would like to ensure your next investment property is in the right market and performs in the way you need it to for your circumstances, please reach out to us at tayloredpropertywealth.com.au. We would love to catch up with you and work together as a team to help you secure your next investment property.

🔥🔥🔥

More information:

➡️Facebook Page – advice and tips

➡️Instagram – more helpful advice