What 3 investment properties will look like in 15 years!

Today we are breaking down what just 3 investment property purchases can look like in a 15 year period from the first purchase. This is not a super aggressive strategy and is something that a lot of everyday Australian’s can achieve.

To keep things simply we have used cash deposit for each of these purchases. The powerful thing is that you can access equity to leverage far more purchases then this scenario has factored.

We have used a conservative 5% yearly capital growth amount and also a 3% annual rental income growth amount. Remember that if you are getting these purchases right, purchasing in areas primed for growth the capital growth and rental income growth will increase at a more rapid rate then these scenarios.

At the end of these scenarios we will break down the passive income amounts, the gross rental yield on the portfolio, the current LVR position(without paying any debt down) and some strategy at this point within the portfolio.

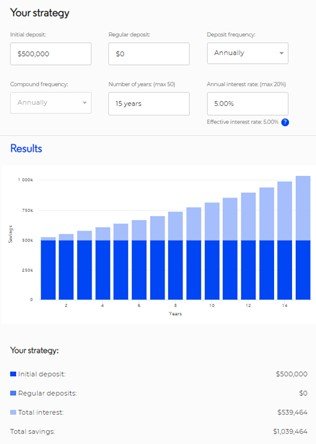

Foundational Property purchase 1

Property was purchased for $500,000 with a 10% cash deposit plus costs.

$450,000 loan held Interest only over the 15 year period, average rate of 5.00% IO.

5% capital growth rate on average over the 15 year period.

At time of purchase the property generated a gross yield of 5% or $480 a week.

3% rental income growth on average over the 15 year period.

Capital growth rate of 5% over 15 year period.

Rental income growth of 3% over a 15-year period.

Numbers after 15 years

Property value now: $1,039,464. $539,464 increase.

$450,000 loan held Interest only over the 15 year period, average rate of 5.00% IO.

Yearly interest only repayments: $22,512

Gross yield now on intial purchase price: 7.77%

Yearly rental income amount: $39,896

Cash surplus: $17,384

LVR:43% – Although the debt hasn’t been paid down the LVR has dramatically dropped due to the increase in property value.

Foundational Property purchase 2(purchased one year after the first property)

Property was purchased for $450,000 with a 10% cash deposit plus costs.

5% capital growth rate on average over the 14 year period.

At time of purchase the property generated a gross yield of 5% or $432 a week.

3% rental income growth on average over the 14 year period.

Capital growth rate of 5% over 14 year period.

Rental income growth of 3% over a 14-year period.

Numbers after 14 years (due to one year after first purchase)

Property value now: $890,969. $440,969 increase.

$405,000 loan held Interest only over the 15 year period, average rate of 5.00% IO.

Yearly interest only repayments: $20,256

Gross yield now on intial purchase price: 7.54%

Yearly rental income amount: $33,956

Cash surplus: $13,700

LVR:45% – Although the debt hasn’t been paid down the LVR has dramatically dropped due to the increase in property value

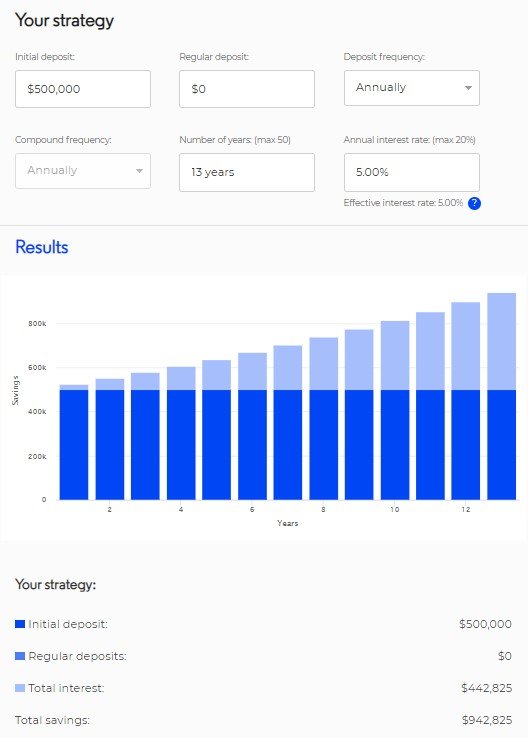

Foundational Property purchase 3(purchased two years after the first property)

- Property was purchased for $500,000 with a 10% cash deposit plus costs.

- 5% capital growth rate on average over the 13 year period.

- At time of purchase the property generated a gross yield of 4.5% or $432 a week.

- 3% rental income growth on average over the 13 year period.

Capital growth rate of 5% over 13 year period.

Rental income growth of 3% over a 14-year period.

Numbers after 13 years (due to two years after first purchase)

- Property value now: $942,825. $442.825 increase.

- $450,000 loan held Interest only over the 15 year period, average rate of 5.00% IO.

- Yearly interest only repayments: $22,512

- Gross yield now on intial purchase price: 7.43%

- Yearly rental income amount: $32,968

- Cash surplus: $10,456

- LVR:47% – Although the debt hasn’t been paid down the LVR has dramatically dropped due to the increase in property value

Portfolio Numbers overall

- Total portfolio Value: $2,873,258

- Total rental income: $106,820

- Total debt value: $1,305,000

- Total Gross Rental Yield on the portfolio based on original purchase prices: 7.58%

- Total portfolio LVR position: 45%

Factors for strategy:

- Over time the portfolio will become positive cashflow, you can then funnel these funds back into either paying some of the current debt down, or hold funds in an offset account which will mean you save interest and ultimately helps pay down more debt. This requires discipline and delayed gratification! This will only improve the cashflow at the end of the 15-year period

- Utilize your yearly tax returns to go straight back onto paying down the debt. This will help reduce some of the debt without using your surplus cash. This requires discipline and delayed gratification! This will only improve the cashflow at the end of the 15-year period

- Use your surplus cash to help pay down existing debt or hold in the offset account. This is surplus cash from your employment. This will be powerful in combination with the surplus cash from the portfolio. This requires discipline and delayed gratification! This will only improve the cashflow at the end of the 15-year period

- You can then sell one of these properties within the portfolio, using the profits to help pay down the debt on the remaining two properties you hold, again creating the portfolio to be more positive cashflow

🔥🔥🔥